In JC’s Newsletter, I share the articles, documentaries, and books that I enjoyed the most in the last week, with some comments on how we relate to them at Alan. I do not endorse all the articles I share, they are up for debate.

I’m doing it because a) I love reading, it is the way that I get most of my ideas, b) I’m already sharing those ideas with my team, and c) I would love to get your perspective on those.

Talent is evenly distributed in the world, but opportunity is not.

When we provide opportunity to places where people don’t normally have it, they tend to be great colleagues, and stay for a really long time.

Payroll management:

We work with international payroll providers.

Also some of these employees are contractors who bill a fixed amount every month.

More simple, especially when you hire just 1 person in a country.

On their side, they usually use a corporation for everything related to taxes and stuff.

➡️ Alan is only in 9 countries but expanding :) We use similar tools.

2️⃣ Attracting profiles

Companies should promote themselves to their user base.

You run ads for your product: run ads for your company. If you have roles to hire, say those. Run an ad for them.

We put Easter eggs all over our products that lead people to our jobs page.

All our “about” pages point people to our hiring.

➡️ I love the idea of leveraging your product more.

3️⃣ Company structure, scaling, and tradeoffs

Automattic is 2,000 people now. 700 new people hired last year.

CEO, HR, legal and systems’ role is to remove barriers and help the rest of the company go faster.

➡️ That is very important!

The teams run like mini companies. They have their own CEOs, executives, and CMOs.

All org structures are a series of tradeoffs. You need to be deliberate about what trade-offs you’re choosing.

Automattic is fractal.

When you zoom in or out, it’s self-similar.

When the entire company was 20 people, it looked a lot like what a team of 20 people looks like now.

There’s a natural growth and division of teams.

4️⃣ Decision-making and transparency

Letting the right people decide

I try to make as few decisions as possible.

Decisions come from the people with the most information. The wisdom is in the people talking to customers, writing the code, designing things, doing user tests.

We push decisions to the teams, the divisions, the edges of the branches of the tree versus the trunk.

None of us are as smart as all of us.

➡️ We push for the same at Alan.

Transparency & documentation

There’s no internal email.

Things are written down, shared, communicated. Decision journals.

Every single decision is on one of these internal blogs.

Future generations or future versions of ourselves can tell why we took this or this decision.

➡️ Exactly the same at Alan where all decisions are written through Github issues/discussions.

Taking decisions / CEO’s input

Take reversible decisions quickly, and irreversible decisions deliberately, or slowly.

Decisions are set into two categories:

Most — 99% — is very reversible.

Some are big — fundings, acquisitions — so we need to be very deliberate.

The things that come to me are the things that no one else has been able to resolve yet.

➡️ I feel the same.

The problem made it through a lot of layers of smart people trying to resolve it before it got to me.

That means that my job is never dull. I see the edge cases, things which you never thought of. They’re completely novel.

6️⃣ Managing an open-source/free product.

“What will be best for the WordPress community this year, 10 years, 30 years from now? What will make us the most sustainable, the most resilient, the most antifragile?”

I align the economic self-interest with the long-term benefits for the community.

Sometimes we need to charge for something.

We have an anti-spam plugin (Akismet).

It’s free for personal use, and paid for commercial use.

It’s kind of an honor system. We don’t really police it. It’s a Robin Hood business model.

A very small percentage of people pay for it, and that percentage makes it sustainable.

I was at Amzn early '00s when we lost 95% of our market cap. Later at FB I negotiated a down-round in '09, and then in '12 our stock dropped 50% post-IPO.

Growth can wait, survival cannot. Amzn’s stock price crossed $100 in '99 and bottomed at $6 in '01 (months from bankruptcy). We cut burn from >$1B to positive free cash flow by raising prices to stop the bleeding. Revenue growth slowed to 3% but we lived to fight another day

Change the tone. Amzn did a small but symbolic RIF in 2000. Around that time, Jeff was presented with a team t-shirt - he threw the team out of his office and banned all company swag. We even removed aspirin from the break rooms, served coffee and water. Small acts set the tone

Every great company overcomes existential threat. A hero must traverse the abyss - nobody chooses it, but everyone eventually faces it. How you respond...that is all that matters

➡️ Good view on the market, and how (if we need to), we will trade-off growth to become cash flow positive.

👉 How Instagram and Twitter buried the hatchet (Plateformer)

Mosseri kept a list of what he called “finally features” — stuff that could be built relatively easily that the user base had been clamoring for. It’s the low-hanging fruit of the product world — stuff like letting everyone add links to their stories, a feature Instagram shipped last week.

“They’re not really a priority to the company strategically, but sometimes you’ve just gotta make time for that kind of work,” he said.

Meanwhile, Mosseri recently held a hackathon to work on more “finally features,” some of which will be shipping soon.

➡️ On the value of Hackathons focused on shipping small delight features once in a while.

That’s why I believe that the wrong board member can break your company faster than the right board member can make it. So when building a board, choose wisely.

For example, when I was first starting LinkedIn, I had a board member who insisted that the core of our business would be advertising. Meanwhile, I saw LinkedIn’s first scale business model as SaaS and subscription-based, which is what turned out to be the case.

A lot of time was spent in the thicket of this struggle – time no entrepreneur really has. The problem wasn’t that the board member disagreed with me. It’s that they disagreed without evidence. They based their assessment on patterns they were already familiar with, instead of on data from the company right in front of them.

Not only was this board member’s past experience not helpful, it was actively harmful to the company, because the board member kept distracting me and the executives with his assertions and requests.

Any board member you’re considering should come with humility about what they do and don’t know.

Starting in the 1990s, Tiger required applicants to complete a 450-question test that took over three hours to complete. It was designed to assess aptitude alongside desirable character traits including competitiveness, intellectual openness, teamwork, and integrity. A former employee recalled one of the test’s questions:

Is it more important to get on well with your team or to challenge them? Would you prefer to be intellectually right but loose money or to be intellectually wrong but save the trade?

Snap said that at least 600 million people use the app at least once per month. It’s is now used by three-quarters of people aged 13 to 34 in more than 20 countries.

Clover referring to itself as a physician enablement company.

It's moving away from the insurance business (hint: growth is slowing and MLRs are terrible) and it's potential as an enablement company.

Babylon showed solid growth in VBC membership but has had terrible MLRs and offered very little concrete to say about how it is managing risk effectively.

Oscar continued its focus on insurance profitability while +Oscar got its first SaaS sale, sounding a lot like a member engagement play.

Hims posted a strong quarter hitting $100 million of revenue in a quarter for the first time. ((release) / (transcript))

The company focused on three core areas of its flywheel driving the growth being 1) new partnerships to drive brand awareness with an emphasis on retail, 2) delivering on that brand awareness with a new app experience delivering more content and cross selling opportunities and 3) driving operational leverage via fulfillment vertical integration.

Relative to its peers (more specifically Ro), Hims & Hers still seems more focused on delivering on the lifestyle/wellness aspect of the brand rather than expanding into some of the more difficult/traditional conditions to treat.

Doesn't seem like a bad place to live for now with its over 700k subscribers to continue developing customer relationships, get to profitability and figure out how far into more in-depth care really makes sense.

CVS Health is the second-largest healthcare company in the world, with a $141B market cap. The company’s main assets include pharmacies, walk-in medical clinics, a pharmacy benefit manager, and a health insurance company.

➡️ They try to be one-stop in some ways.

Behavioral health getting Real. Therapist-driven behavioral health platform Real brought in $37M from a Series B round led by Owl Ventures. The money will be used to create new therapist-designed Pathways and educational materials.

Cerebral was unfortunately in the news a bunch again this week, first for halting the prescription of controlled substances to new and existing patients, and second for the Board firing the CEO.

👉 Babylon: Capital Markets Day - 23 May 2022 (Babylon)

➡️ Babylon is the proof of our first principles. If you are not the insurance company, then you need them to pay you.

We reduce Emergency Room visits by over 25% as show by independent Ipsos Mori study

And create acute care cost savings of up to 25% as proven in a peer-reviewed study of NHS data

➡️ Impressive revenue growth.

80% recall, on average, achieved by our AI compared to 83.9% recall by doctors taking the same test

A combination of $3-4bn of value based care revenue at 7.5-10% average gross margin, and $150-200m of licensing revenue at ~90% margin could allow us to breakeven

➡️ Interesting to see their margin.

➡️ We could think how to expand data sources.

Adjusted EBITDA guidance to be a maximum loss of $(295)m at $1.0bn revenue

Adjusted EBITDA and cash flow breakeven no later than 2025

Sufficient cash to fund 2022, and continuing to pursue funding options for the long term.

➡️ Very high-burn, and likely will be hard for them to finance at the end of the year? I hope they’ll succeed.

Babylon Health's stock price dropped almost 53% on Friday, the day after its investors lock up period expired post-SPAC six months ago. Generally it doesn't seem like a good sign for the business when inside investors are all looking to exit their positions so quickly that they tank the stock price by 50%+ in a day because they're looking to sell so many shares. Link

➡️ They are now valued at $435m.

NexHealth, an API that helps dental practices with digital patient engagement, raised $125 million at a $1 billion valuation. It's pretty wild to see that they're doing around $5 million of revenue currently (per this tweet from a co-founder) and yet somehow is still being valued at $1 billion. We'll see how quickly they can expand beyond the dental market. Link

➡️ Interesting benchmark.

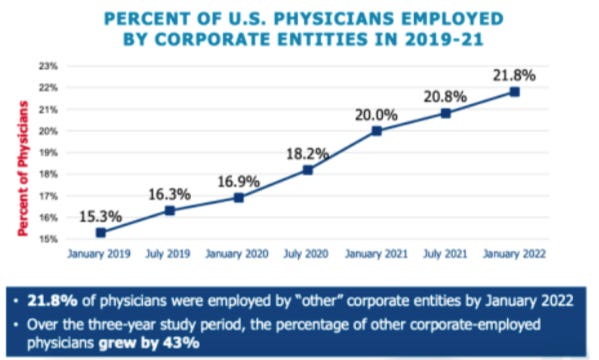

PAI released a report on physician employment trends. The chart below is striking with the number of corporate-employed physicians growing by 43% over the last three years. Link

➡️ Interesting number. Does it apply to Europe too?

It’s already over! Please share JC’s Newsletter with your friends, and subscribe👇

Let’s talk about this together on LinkedIn or on Twitter. Have a good week!